Seamless Execution from Origin to Destination: Integrating CIF/FOB Strategy with End-to-End Trade Finance

Introduction: The Integrated Trade Cycle

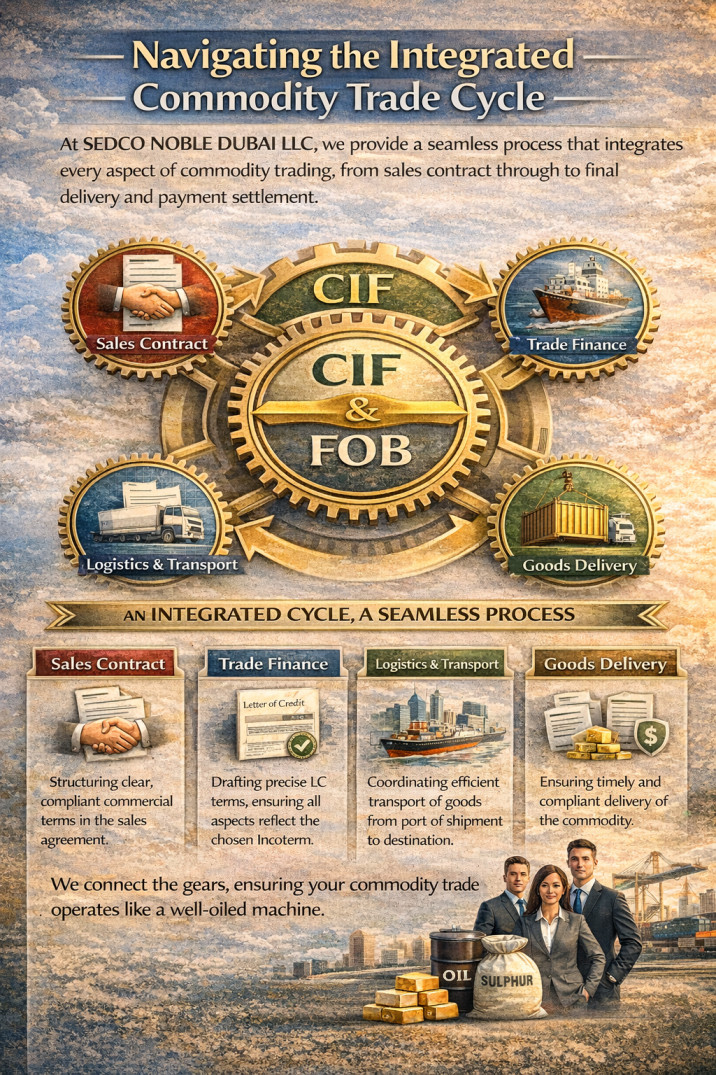

A successful commodity transaction is a seamless loop, where commercial terms, physical logistics, and financial instruments are not separate components, but interlocking gears. The choice between CIF (Cost, Insurance, and Freight) and FOB (Free On Board) sets the initial gear in motion, determining the division of responsibilities. The true test, however, lies in expertly integrating this choice with the entire trade finance and execution machinery. At SEDCO NOBLE DUBAI LLC, we specialize in managing this integrated cycle, providing a single point of accountability from the sales contract through to final delivery and payment settlement.

Part 1: The Execution Chain – Connecting Terms to Action

Our process ensures the chosen Incoterm is actively executed, not just written into a contract:

For FOB (Buyer-Controlled Shipment) Transactions:

Post-Contract Activation: Once an FOB term is agreed, our logistics coordination team (or trusted partner network) assists in executing the buyer's responsibilities: vetting and booking reliable carriers, arranging for adequate insurance beyond minimum clauses, and coordinating the load port logistics.

Document Orchestration: We ensure all documents generated from these buyer-led actions (e.g., the forwarder's bill of lading, the insurance certificate) are per-aligned with the strict requirements of the Letter of Credit we have structured, preventing discrepancies.

Finance Alignment: We ensure the LC payment trigger is correctly tied to the presentation of these buyer-procured documents, and that any advance payments for freight are managed securely.

For CIF (Seller-Arranged Shipment) Transactions:

Seller Performance Monitoring: While the seller arranges freight and insurance, we conduct due diligence on their chosen carriers and verify the adequacy of the insurance coverage for the specific commodity (e.g., confirming sulphur is not excluded, or gold has all-risk coverage).

Proactive Document Review: We often obtain drafts of the seller's bill of lading and insurance certificate before shipment to pre-check for compliance with the LC terms, avoiding nasty surprises at the presentation stage.

Cost Verification: We help clients verify that freight costs quoted under CIF are market-competitive, ensuring the delivered price remains fair.

Part 2: Our End-to-End Management Framework Regardless of the Incoterm, our service provides a comprehensive overlay of security and management:

Phase 1: Structuring & Onboarding

Incoterm Advisory: Collaborative selection of CIF or FOB based on your risk tolerance, logistics capability, and cost targets. Instrument Design: Drafting of LCs, SBLCs, or payment guarantees with terms that perfectly reflect the chosen Incoterm and the specific commodity's handling needs.

Compliance Bridge: Conducting KYC/AML checks and ensuring the entire structure meets DFSA (DIFC) and international regulatory standards from day one.

Phase 2: Operational Execution & Monitoring

Logistics Oversight: Continuous communication with agents at load and discharge ports, tracking vessel movement, and monitoring key milestones (loading, sailing, arrival).

Documentary Control: Meticulous preparation, collection, and presentation of all required documents (commercial invoices, certificates of origin, weight and quality certificates, transport documents) under the LC.

Quality & Inspection Management: Appointing and coordinating with independent inspection companies (like SGS or Inspectorate) for pre-shipment survey and assay, a non-negotiable step for sulphur and gold trades.

Phase 3: Financial Settlement & Closure

Presentation & Payment: Presenting the fully compliant document package to the bank and managing the payment process until funds are received.

Discrepancy Resolution: If a documentary issue arises, our experts intervene immediately to negotiate a resolution with banks and counterparties to prevent payment delays.

Post-Transaction Analysis: Reviewing the deal performance to identify efficiencies for future transactions.

Part 3: The Unique SEDCO NOBLE Value: Partnership Capital in Action

This end-to-end service is supercharged by our investment partnership model. When we invest alongside you, our commitment to flawless execution is existential. Every detail—from the correctness of the bill of lading to the timeliness of the inspector—matters directly to our own bottom line. This alignment ensures an unmatched level of diligence and proactive problem-solving throughout the CIF/FOB execution chain.

Conclusion: One Partner for the Entire Journey

In global commodity trading, fragmentation of responsibility is the primary source of risk and cost overruns. Handing off the Incoterm decision to a commercial team, the LC to a bank, and the logistics to a separate agent creates dangerous gaps.

SEDCO NOBLE DUBAI LLC closes these gaps. We provide integrated expertise that connects the commercial (CIF/FOB), financial (LC/SBLC), and physical (logistics/inspection) realms into one coherent, managed process. We offer not just a financial instrument, but a guaranteed pathway for its successful execution.

Let us manage the complete loop, so you can secure the profitable outcome.

Join the Conversation (7)

Leave a Comment

No account required! Just enter your name and email.

The write-up from SEDCO NOBLE DUBAI LLC states that their logistics team (or trusted partners) assists the buyer by "arranging for adequate insurance beyond minimum clauses" as part of executing the buyer's responsibilities in FOB transactions. This implies the additional/enhanced insurance (e.g., broader all-risk coverage instead of basic/minimum clauses) goes beyond what might be a minimal or default level, but it remains the buyer's responsibility to cover the cost.

In practice:

Standard FOB does not require any mandatory insurance from either party, but buyers typically purchase it to protect their interest since they bear the risk post-loading.

If "minimum clauses" refers to basic coverage (similar to how CIF sellers provide only minimum under Institute Cargo Clauses C), then any upgraded or "adequate" coverage arranged by SEDCO NOBLE's team is still funded by the buyer, as it's fulfilling the buyer's duty under FOB.

The company's role appears to be facilitative—vetting, coordinating, and securing better protection on the buyer's behalf—rather than absorbing the premium cost themselves. This aligns with their overall service as an integrated partner managing buyer-led actions without shifting core financial responsibility.

If this is part of a client discussion, you could clarify directly with SEDCO NOBLE whether they offer any cost-sharing, subsidies, or bundled pricing for such arrangements in specific deals, especially under their investment partnership model.

Key reasons:

Under FOB, the seller's obligations end at loading the goods on board; they have no duty to provide or fund insurance for the main carriage.

Insurance is not mandatory in FOB, but buyers almost always purchase it to protect their interest since risk transfers to them at the load port.

Any "beyond minimum" upgrades arranged via SEDCO NOBLE's support are part of executing the buyer's responsibilities, not shifting the premium cost to the seller or the company itself.

Their role is facilitative and value-added (coordination, vetting for reliability, ensuring LC compliance), aligning with their integrated service model—especially under the investment partnership where aligned incentives drive diligence, but core costs like insurance premiums stay with the buyer unless explicitly negotiated otherwise in a deal.

In practice, buyers often prefer this "adequate" enhanced coverage to reduce exposure, and the premiums reflect the upgraded scope (potentially higher than basic policies). If SEDCO NOBLE bundles any related fees or offers cost offsets via their partnership model (e.g., in co-invested deals), it would be case-specific and worth confirming directly with them.

For sulphur or gold trades (their focus areas), comprehensive insurance is especially critical due to high value and risks, making buyer-funded enhancements common to avoid under-insurance issues.

At SEDCO NOBLE DUBAI LLC, we take a thorough, multi-layered approach to verify the adequacy of the marine cargo insurance policy (typically provided by the seller in CIF terms) and its alignment with the LC requirements. This process draws on our operational heritage in high-stakes environments and our deep DIFC-based banking/logistics network. Here's how we handle it step by step:

1. Pre-Shipment Review & Adequacy Check

We require the seller to submit the full insurance policy or certificate (not just a summary) well in advance of loading/shipment.

Coverage verification:

Minimum: At least Institute Cargo Clauses (C) as standard under CIF Incoterms 2020 (covering major perils like fire, stranding, sinking, collision), but for high-value/sensitive commodities we insist on upgraded coverage (e.g., Clauses (B) or (A) "all risks" where appropriate) to address specific risks—such as theft/pilferage for gold, or moisture/damage/contamination for sulphur.

Insured amount: 110% of the CIF value (invoice + freight + insurance) as required under standard Incoterms and most LCs.

Duration: "Warehouse to warehouse" or at minimum from port of shipment to port of destination, including any customary extensions for delays.

Insurer quality: Issued by a reputable, internationally recognized insurer (e.g., A-rated or better per A.M. Best/equivalent), acceptable to major correspondent banks. We cross-check ratings and exclude lesser-known providers if needed.

Commodity-specific tailoring: For gold/precious metals, we ensure explicit coverage for theft, mysterious disappearance, and war/terrorism risks (if route-dependent). For sulphur/energy products, we verify coverage for inherent vice exclusions are minimized and pollution/contamination perils are addressed.

2. Compliance with Letter of Credit (UCP 600 Alignment)

We cross-reference every detail against the LC's insurance clause (typically Article 28 of UCP 600):

Document form: Original policy/certificate (broker's certificate acceptable if countersigned by insurer/agent).

Risks covered: Must match or exceed LC-specified perils (no narrower coverage).

Currency & amount: Matches LC currency; no under-insurance.

Endorsement/assignability: Blank-endorsed or assignable to buyer/applicant (or our financed structure) for claim rights.

Date & issuance: Issued and dated no later than shipment date; covers transit from loading.

No discrepancies: We flag common LC pitfalls like missing "all risks" wording (if required), improper insurer description, or failure to waive subrogation rights against buyer/carrier.

If any gap exists, we work with the seller (and their insurer) to amend/obtain endorsements before documents are presented—preventing LC discrepancies that could delay payment or trigger rejection.

3. Independent Verification & On-Ground Oversight

We engage trusted partners (e.g., inspection firms like SGS/Intertek, or our network of marine surveyors) to:

Confirm policy authenticity directly with the insurer (via email/phone verification).

Review claims history or insurer track record for similar commodities/routes.

For high-value deals (e.g., gold dore or large sulphur parcels), we may require a marine surveyor report or pre-shipment endorsement confirming policy adequacy.

Real-time monitoring: If issues arise (e.g., vessel deviation, delay), our Dubai team coordinates with insurers for extensions or notifications.

4. Final Integration into Transaction

Only once verified do we proceed with financing/structuring (e.g., co-investment, SBLC facilitation).

This ensures the buyer (and our partnership) has enforceable protection, minimizing exposure in volatile markets.

This rigorous process—rooted in our "driller's discipline"—helps avoid the common pitfalls that lead to claims denials or LC rejections, giving our clients peace of mind and faster, smoother executions.

If you're working on a specific CIF sulphur, gold, or energy transaction right now, we'd be glad to review the proposed insurance details (or LC terms) confidentially and provide tailored feedback on adequacy/compliance—no obligation, of course.

Please share more if you'd like us to dive deeper!