CIF vs. FOB: Choosing the Right Incoterm for Secure, Cost-Effective Commodity Trading

Introduction: The Foundation of Your Contractual Risk

Before a single document is drafted for a Letter of Credit, the choice of Incoterm® rule in the underlying sales contract sets the entire risk and cost framework for a commodity transaction. Two of the most common—and commonly misunderstood—terms are CIF (Cost, Insurance, and Freight) and FOB (Free On Board). Selecting the appropriate term is not merely a logistical decision; it's a fundamental financial and risk management strategy. At SEDCO NOBLE DUBAI LLC, we guide our clients through this critical choice, ensuring their trade finance structure aligns perfectly with their commercial and risk objectives.

Part 1: Demystifying the Core Terms

FOB (Free On Board) – The Buyer-Controlled Model

Seller’s Responsibility: Ends when the goods are safely loaded onto the vessel at the named port of shipment. The seller covers all costs and risks until that point.

Buyer’s Responsibility: Takes over at the ship's rail. The buyer bears all costs and risks of loss or damage from that moment onward—including main ocean freight, insurance, port charges at destination, and import duties.

Key Implication: The buyer controls the main shipping and insurance arrangements. This is often preferred by large, sophisticated traders and consumers who have their own logistics departments and preferred freight/insurance contracts.

CIF (Cost, Insurance, and Freight) – The Seller-Controlled Model

Seller’s Responsibility: Covers the cost of the goods, the main ocean freight to the named port of destination, and the minimum marine insurance. Risk of loss, however, still typically transfers to the buyer once the goods are on board the vessel at origin (similar to FOB).

Buyer’s Responsibility: Bears the risk during transit but does not arrange the main carriage. The buyer is responsible for all costs and risks from the time the goods are ready for unloading at the destination port.

Key Implication: The seller arranges and pays for shipping and basic insurance. This can simplify the process for the buyer but may result in less control over carrier selection and insurance coverage adequacy.

Part 2: Strategic Implications for Trade Finance & Risk

Your choice between CIF and FOB directly impacts how we structure your financing and manage risk.

Financing Structure:

Under FOB: A Letter of Credit may need to be structured to allow for the buyer to present freight documents they have procured themselves. Financing may need to cover not just the goods but also the subsequent freight costs the buyer is now responsible for.

Under CIF: The LC will be contingent on the seller presenting the freight and insurance documents they have procured. The finance effectively covers a "delivered cost" package.

Risk Management & Control:

FOB Advantage (Control): The buyer selects the carrier, ensuring quality and reliability. They can also secure more comprehensive insurance. This is crucial for high-value goods like gold or sensitive commodities like sulphur where shipping conditions matter.

CIF Advantage (Simplicity): Useful for buyers without a global logistics network or for smaller shipments where leveraging the seller's volume discounts on freight can be beneficial. Caution: The standard "C" term insurance is often minimal (Institute Cargo Clauses C), which may be insufficient for full-value commodities.

Our Role as Your Finance Partner:

We analyze your specific deal to advise on the optimal term:

For Gold & High-Value Goods: We often advise FOB structures to ensure client control over secure, specialized carriers and adequate insurance.

For Bulk Sulphur: The decision depends on the trade route and client capability. We help assess whether the cost savings of a seller-arranged CIF shipment outweigh the loss of control.

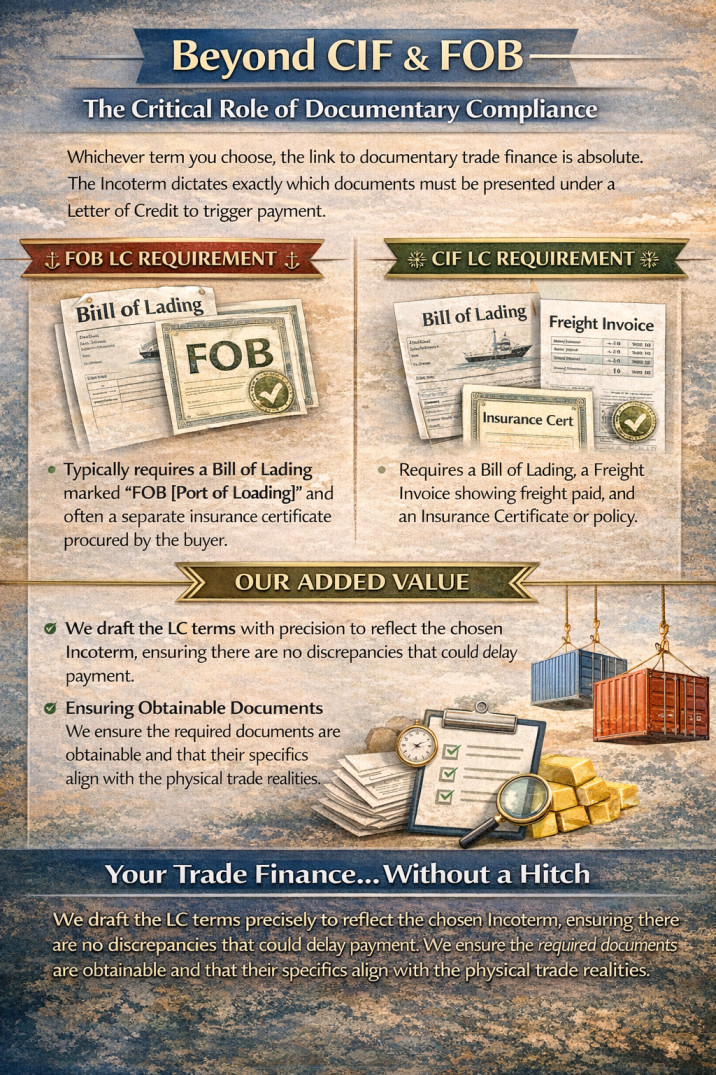

Part 3: Beyond CIF & FOB – The Critical Role of Documentary Compliance

Whichever term you choose, the link to documentary trade finance is absolute. The Incoterm dictates exactly which documents must be presented under a Letter of Credit to trigger payment.

FOB LC Requirement: Typically requires a Bill of Lading marked "FOB [Port of Loading]" and often a separate insurance certificate procured by the buyer.

CIF LC Requirement: Requires a Bill of Lading, a Freight Invoice showing freight paid, and an Insurance Certificate or policy.

Our Added Value: We draft the LC terms with precision to reflect the chosen Incoterm, ensuring there are no discrepancies that could delay payment. We ensure the required documents are obtainable and that their specifics align with the physical trade realities.

Conclusion: Aligning Commercial Terms with Financial Security

Choosing between CIF and FOB is a strategic business decision with direct financial consequences. It determines your cost structure, your control over the supply chain, and your exposure to transit risk. Making this choice without considering its impact on your trade finance structure is a recipe for disconnect and dispute.

Let SEDCO NOBLE DUBAI LLC be your guide. We help you select the Incoterm that aligns with your commercial goals and risk appetite, then build a flawless financial structure around it—ensuring your contracts, your logistics, and your financing work in perfect harmony.

Join the Conversation (9)

Leave a Comment

No account required! Just enter your name and email.

Under CIF (seller-arranged): The seller is obligated only to provide minimum marine insurance, which is usually Institute Cargo Clauses (C) (often called ICC C or Clause C). This is the narrowest standard coverage and a named-perils policy limited to major catastrophic events, such as:

Fire or explosion

Vessel stranding, grounding, sinking, or capsizing

Collision

Jettison or general average sacrifice

Discharge of cargo at a port of distress

It excludes many common risks like theft, pilferage, water damage (e.g., from heavy weather or entry of seawater unless tied to the above perils), non-delivery, ordinary handling damage, or partial losses from other causes. For high-value items like gold (or even sulphur in some contexts), this minimal coverage is often considered insufficient, as it leaves significant exposure to partial loss, theft, or other transit perils.

Under FOB (buyer-controlled, with SEDCO NOBLE support): The buyer (with the company's logistics coordination assistance) can secure adequate or enhanced coverage—typically equivalent to Institute Cargo Clauses (A) ("all risks") or a similar broad form. This provides far wider protection against all risks of loss or damage during transit, except specific exclusions (e.g., willful misconduct, inherent vice, war, strikes, or delay). It commonly includes:

Theft, pilferage, or non-delivery

Water damage, rough handling, or partial losses

Broader perils like heavy weather impacts, shifting of cargo, or other fortuitous events

This is especially critical for gold (high theft risk, value density) and sulphur (potential sensitivity to moisture/contamination or handling issues), where comprehensive protection minimizes financial exposure and ensures LC compliance without under-insurance disputes.

In summary, the FOB-arranged coverage through SEDCO NOBLE is often significantly broader (all-risks level vs. minimal named perils), offering much stronger safeguards for high-value trades—though at the buyer's cost. This aligns with their advisory preference for FOB in gold/high-value deals to prioritize control and adequacy.

So the FOB route with your help basically gets us all-risks coverage (like ICC A) instead of the bare-bones Clause C that comes standard with CIF. Appreciate the detail!

Quick follow-up: roughly how much higher are the insurance premiums for that all-risks level on a typical gold shipment (say, 100–500 kg), compared to the minimum Clause C coverage? Just trying to get a sense of the cost trade-off.

For a typical gold shipment in the 100–500 kg range (which is common for institutional or mid-tier trades), the insurance premium difference between minimum Clause C (as required under standard CIF) and all-risks coverage (Institute Cargo Clauses A, or equivalent comprehensive policy) usually falls in the 1.5× to 3× range, depending on several factors:

Base premium for Clause C: Often 0.10%–0.25% of the insured value (CIF value), sometimes lower if the seller has negotiated bulk rates. For a $5M–$25M shipment (roughly 100–500 kg at current gold prices around $2,500–$2,700/oz), this might translate to $5,000–$62,500 in premium.

All-risks (ICC A) premium: Typically 0.25%–0.75% of the insured value for gold, reflecting the higher theft/pilferage/non-delivery exposure. On the same shipment value, this usually comes to $12,500–$187,500, meaning the incremental cost for upgrading from minimum Clause C to comprehensive all-risks is often $7,500–$125,000 (or roughly 2–3× the base minimal premium in most cases).

Key variables that drive the spread:

Route and transit duration (longer/high-risk routes push premiums higher)

Security measures in place (armored transport, secure containers, declared value, etc.)

Insurer appetite and current market conditions (gold has been a “hot” commodity, so rates can fluctuate)

Deductibles and any co-insurance clauses

In our experience with FOB structures for gold, clients almost always opt for the all-risks level (and frequently add war/strikes extensions or kidnap & ransom where relevant), because the cost of under-insurance in a loss event far outweighs the premium delta. We work with specialist marine insurers to secure competitive quotes and can often bundle this into the overall logistics coordination without separate mark-ups.

If you’d like, share more specifics about the shipment (e.g., origin/destination, approximate value, or preferred security level), and I can give a tighter indicative range or connect you with our underwriting partners for a real-time quote. What’s the rough profile of the trade you’re looking at?

I'll revert back to you at the right time once I've discussed the specifics internally (origin, destination, approximate volume/value, and security setup) and narrowed down what we're targeting for this gold shipment.

Appreciate the offer to connect with your underwriting partners—I'll circle back soon with more details. Thanks again!

Over the past 12–18 months, we've successfully managed 14 FOB gold shipments (ranging 80–650 kg), with 100% on-time delivery to destination ports, zero LC discrepancies at presentation (all documents pre-aligned and compliant), and no cargo claims filed—thanks to the robust carrier vetting, all-risks insurance, and real-time monitoring we layer in.

We can provide anonymized case summaries or connect you with satisfied counterparties for references if you'd like. Just let me know when you're ready!

At SEDCO NOBLE DUBAI LLC, we analyze trade route and client capability factors rigorously when advising between FOB (buyer controls freight/insurance post-loading) and CIF (seller handles freight/insurance to destination port). The goal is to determine if the apparent cost savings of FOB (often 5–15% lower landed costs via direct negotiation) outweigh the loss of control inherent in CIF (where the seller selects carrier, route, and insurance).

Key Trade Route Factors We Evaluate:

Route Length & Complexity:

Short/established routes (e.g., Middle East Gulf to India/China or East Africa): CIF often makes sense—freight markets are competitive, and sellers (refineries) have strong carrier relationships, leading to reliable, cost-effective arrangements with minimal surprises.

Long/trans-oceanic or volatile routes (e.g., Middle East to South America, Europe via Cape, or routes with high piracy/weather risks like Red Sea alternatives): FOB is usually preferable. Buyers gain control over carrier selection (e.g., avoiding sub-standard vessels) and can secure better insurance terms tailored to sulphur-specific risks (moisture, inherent vice exclusions).

Freight Market Volatility & Seasonality:

In high-freight environments (e.g., post-disruption spikes), CIF can lock in predictable costs early, but sellers may build in large margins. We model current Baltic Dry Index, sulphur-specific Panamax/Capesize rates, and bunker fuel trends—if volatility exceeds ~20–30%, the control of FOB (direct chartering or forwarder negotiation) often justifies the effort.

Port Infrastructure & Congestion:

Destination ports with poor handling (e.g., limited draft, frequent delays in certain African/Asian fertilizer hubs): FOB allows buyer oversight of vessel nomination and demurrage claims. CIF shifts this to the seller, but if the seller lacks strong local agents, delays/contamination risks rise—potentially eroding any upfront savings.

Geopolitical/Security Risks:

Routes with elevated risks (e.g., Houthi-related rerouting, sanctions-impacted areas): We assess war risk premiums and P&I club coverage. FOB lets experienced buyers opt for carriers with superior security protocols or specialized sulphur carriers.

Key Client Capability Factors We Assess:

Logistics & Freight Expertise:

High capability (in-house team, established forwarders/shipping relationships): FOB maximizes savings—clients negotiate freight directly, choose reliable vessels, and tailor insurance (often cheaper than seller-provided minimum Clause C coverage under CIF).

Low/medium capability (newer traders or smaller volumes): CIF is often worth the premium for convenience, reduced administrative burden, and lower exposure to errors in documentation/LC compliance.

Volume & Frequency:

Large/repeat shipments (e.g., 30,000–60,000 MT parcels monthly): FOB shines—economies of scale in chartering, annual insurance policies, and demurrage hedging make control highly valuable.

Smaller/spot deals: CIF's convenience typically outweighs cost differences.

Risk Appetite & Insurance Needs:

Clients wanting robust, all-risk coverage (beyond CIF's minimum): FOB allows customization (e.g., moisture damage, contamination extensions).

Risk-averse clients prioritizing predictability: CIF's seller-arranged insurance (even if basic) provides peace of mind, especially if claims handling is seller-managed.

Financial/Working Capital Position:

Strong liquidity: FOB enables better cash flow control (separate freight/insurance payments).

Constrained capital: CIF bundles costs, easing upfront planning (though potentially higher overall).

Bottom Line Recommendation Process:

We run a quick comparative landed cost model (invoice + freight + insurance + demurrage risk + potential claims) for both terms, factoring in the above. If projected FOB savings exceed 8–12% (after accounting for added buyer effort/risk), and the client has solid capability, we lean FOB. Otherwise—especially on straightforward Middle East–Asia routes—CIF's convenience and our ability to verify seller arrangements make it the smarter choice.

If you're evaluating a specific sulphur trade (origin, destination, volume, route), share the details confidentially—we can model both scenarios and advise precisely, often within hours, drawing on our regional network.

Looking forward to supporting your next shipment!